I am NOT a financial advisor. I wrote this for entertainment purposes. Please consult a financial professional. Or do your own research before making any financial decisions.

In a report published on January 25, 2023, from Bankrate, 43% of Americans would cover the cost of a $1,000 emergency using their savings. A quarter of those surveyed would use a credit card to cover the $1,000 emergency.

They asked people, “How would you pay for a surprise expense?”. They used a $1,000 emergency room visit or car repair as the example.

Here is the table of their findings (per Bankrate’s website):

The findings aren’t surprising. Lower income families don’t have the savings to rely upon to cover such a cost.

While higher income households are comfortable reaching into savings.

Instead of telling you how I feel about economic surveys, I will tell you how my wife and I dealt our own surprise expense.

The Dilemma

While picking up a friend from LAX, our car died on us. That was the first and hopefully only time I pick up a friend in a tow truck.

As an amateur mechanic, I looked over our poor broken down car and we decided it was time to move on. It had over 253,000 miles on it and had developed a couple new creaks and rattles.

We decided it was time to move on.

Like many people, we found the new car market to be ridiculous at this time. There were crazy markups, limited selections, and buyers had no say in any of the negotiations.

The used car market wasn’t much better, but we felt we could find something to hold us over in the meantime.

The Purchase

We decided to purchase a 2006 Mini Cooper with 80k miles on it for $9,000 after taxes and fees.

We charged our new sunshine orange convertible to my credit card.

Before buying the car, we knew our credit union was running a balance transfer promotion.

The Balance Transfer Promotion

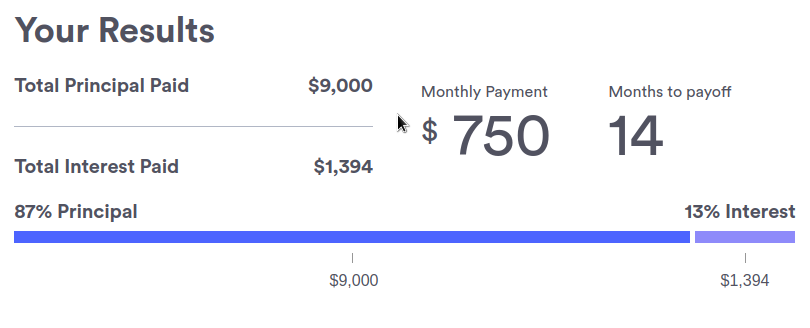

My credit card has an APR of 24%. Paying $750 a month, the balance could be paid off in 14 months but we would still pay over $1,300 of interest.

We needed another option.

At that time our credit union was running a balance transfer promotion.

Balance transfer offers frequently include interest free periods. So explore your options.

Our credit union was offering members a 12-month interest free period.

They were also allowing members to transfer a credit card balance to their credit union credit card for free. Yes, for $0 you could transfer a balance.

Most banks charge a transfer fee of $5 or 3% of the transfer amount, whichever is higher, of course.

Obviously, we could only transfer up to the credit limit of the credit union credit limit, and the credit union would need to approve it. Our balance transfer approval went through the same day.

The transfer itself took a few days, about 3 days to go through.

In the end, we had transferred the entire balance of $9,000 from my bank credit card to my credit union credit card.

The Credit Score Dive

The credit utilization percentage jumped from 3% to 15% and my credit score plummeted by a total of 87 points. This was due to the purchase and transfer being reported on both of the credit cards.

A month later, the balance settled and my bank credit card didn’t show the $9,000 charge.

My credit score jumped back up by 30 points.

None of this spooked me or had me worried.

Credit scores are temporary. Their movements are predictable and not difficult to understand.

I was now using above the “Excellent” credit utilization percentage which is less than 10% of my total credit. Not a big deal, if we stuck to our payment plan going forward.

The Payment Plan

By planning out our finances, we knew we would be able to pay off the balance within the year.

This was very important, as the credit union’s balance transfer had a 0% interest rate for the first year, or the next 12 months.

Like I said earlier, this is common so look at what your bank or credit card offers for interest free periods.

Nerdwallet does a great job of showing the latest offers on the market. They mostly list large banks, so I recommend check your local credit unions for offers.

At first we were paying a few hundred dollars more than the minimum payment, which was established by the credit union.

Throughout the year, as we were able to increase our income, with new jobs and a promotion, we increased our monthly payments.

As the balance shrank, my credit score slowly recovered.

As we began to pay more of it off, my credit score started jumping up. Eventually my credit score was back over 800.

I was continuing to use my other credit card for everyday purchases so at times, it was a balancing act, between aggressively paying down the balance and monitoring my day to day spending.

Fast forward to January 2023, we made the final payment on the $9,000 balance. Our plan worked out as we had outlined it.

We are grateful we didn’t have any unexpected emergencies or other large unplanned purchases during the year.

We didn’t pay any interest over the 10 and a half months it took to pay the balance off.

My advice

Step one would be to see what are your credit union options near you. Be sure to ask them about balance transfer offers.

Bankrate has a Credit Card Balance Transfer Calculator that could help you plan. I don’t think it does the “previous minimum payment” math correctly. For that, I would recommend you use their Credit Card Payoff Calculator.

Be on the lookout for that small print!

There is a balance transfer fee charged by the bank or credit union you are moving your money to.

On a $1,000 transfer that would be a $30 fee. That’s not terrible, but on a $9,000 balance transfer that would be $270. That’s a lot less than the potential interest but still an annoying cost.

The more you know, the less stressful the process will be.

Benefits of Balance Transfers

There are some big benefits of a balance transfer, when executed well.

Remember, transferring a balance does not free up more room for you to spend money.

It does allow you to make payments on your terms, but you still need to pay the balance off in full.

Sometimes, we just need some time to catch our breath and get our finances in order.

Creating a budget, yes we have all heard this a thousand times, will give you a clearer understanding about how much you can afford to pay each month.

To take advantage, I recommend maintaining or decreasing your spending habits. The goal is to pay off the balance without accruing any interest.

Questions to Ask Yourself

- Imagine if your credit score dropped by 100 points for the next year, how would that affect you?

Credit scores are used for loan applications as well as some rental lease applications.

- Are you planning to apply for a loan within the year?

A low credit score will result in a high interest rate.

- Do you have a safety net?

Having savings that could pay for some of, if not all your expenses for a month or two should things fall apart is good to have. I recommend keeping this emergency fund in a High Yield Savings Account.

- Can you afford the minimum payment?

We had a $250 minimum payment on our balance transfer. We didn’t know the amount until after we transferred the balance.

Paying only the minimum balance, we would have only paid down $3,000 of the $9,000 balance in the 12 month interest free period. After that, we would have been left with $6,000 at an interest rate of 12%. Yikes!

- How much per month would it take to pay it off within the interest free period?

Do the math. The minimum monthly payment will NOT equal paying the balance off in full within the year.

Divide the total balance transfer by the interest free period, for us it was 12 months.

So 9,000 divided by 12 equals 750.

Again, we drew that into our outline and planned for that monthly expense. As our budget allowed us, we increased our monthly payments.

- Can you afford a high monthly payment without straining your other expenses?

If things are to go sour, would you be able to maintain the minimum monthly payment, while paying for your everyday expenses?

Paying the minimum monthly payment will prevent any interest from accruing, but only for the interest free period. This information can be found in the small print of the balance transfer details. After that, you will be stuck with credit cards with a much higher interest rate.

Checklist

I think by having the items below, you will be in a strong financial position to use a balance transfer.

- 2 credit cards (My example was 1 bank credit card and the other was a credit union credit card)

- Available credit limit (You’ll need the necessary available credit to complete the transfer)

- Safety net (I recommend at least a month’s worth of expenses saved up. The more, the better)

- Develop a payment plan (What is the minimum monthly payment? How much per month will I need to pay off the balance within the interest free period?)

- High enough credit score (Your credit score will take a hit, are you prepared for that?)

Conclusion

I hope this provides you with some insight on balance transfers. A balance transfer can be a great financial tool to help with unexpected large purchases. Even things like replacing large appliances or car repairs.

You know your finances best. Always research and understand the risks involved with credit cards and bank fees.

Budgeting and planning ahead will set you up for success.